Case study2024BST Consulting

ORR Platform.

Standardising how banks rate the obligors on their credit book.

- Period

- 2024 to 2025

- Role

- Programme Manager

Snapshot.

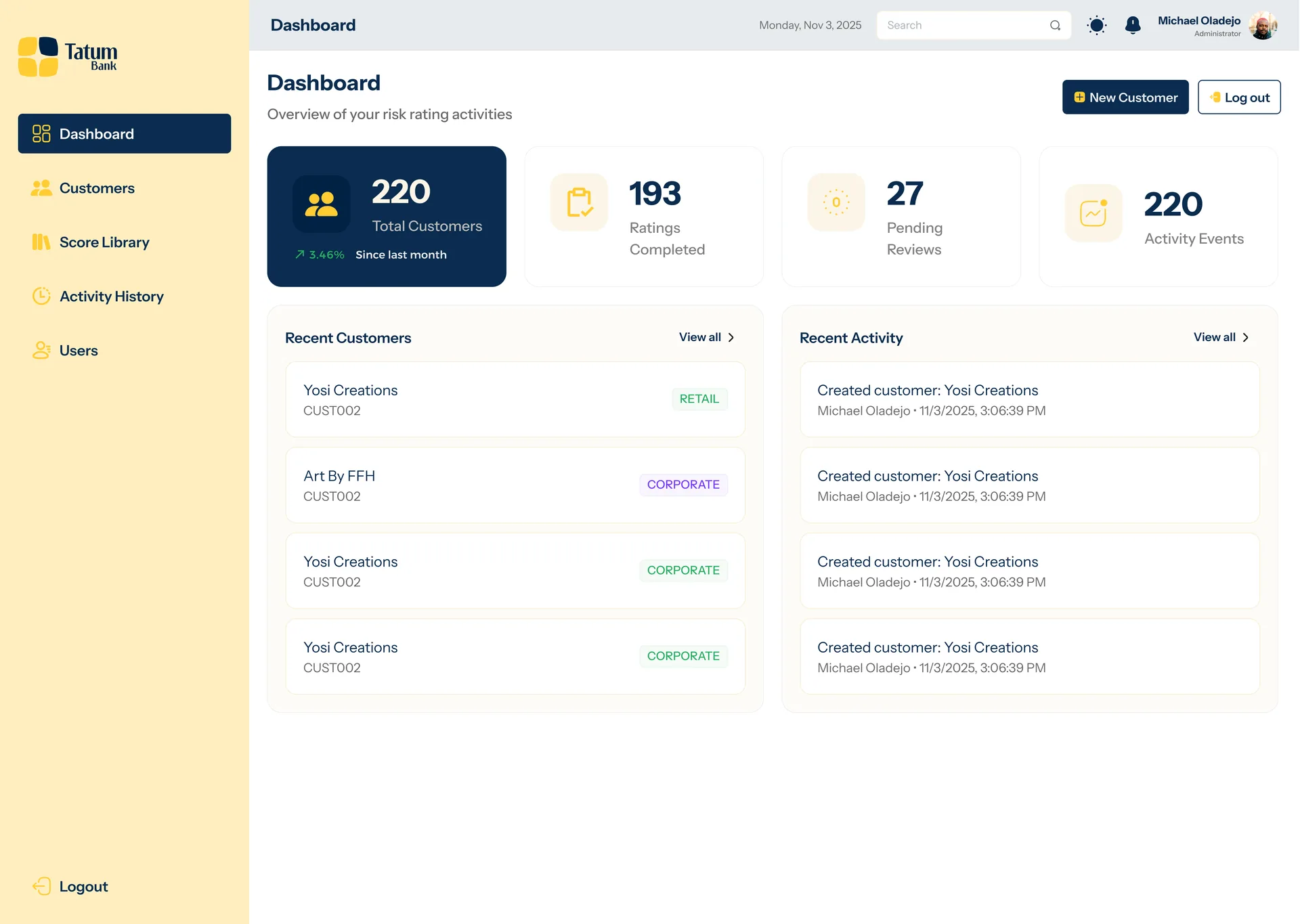

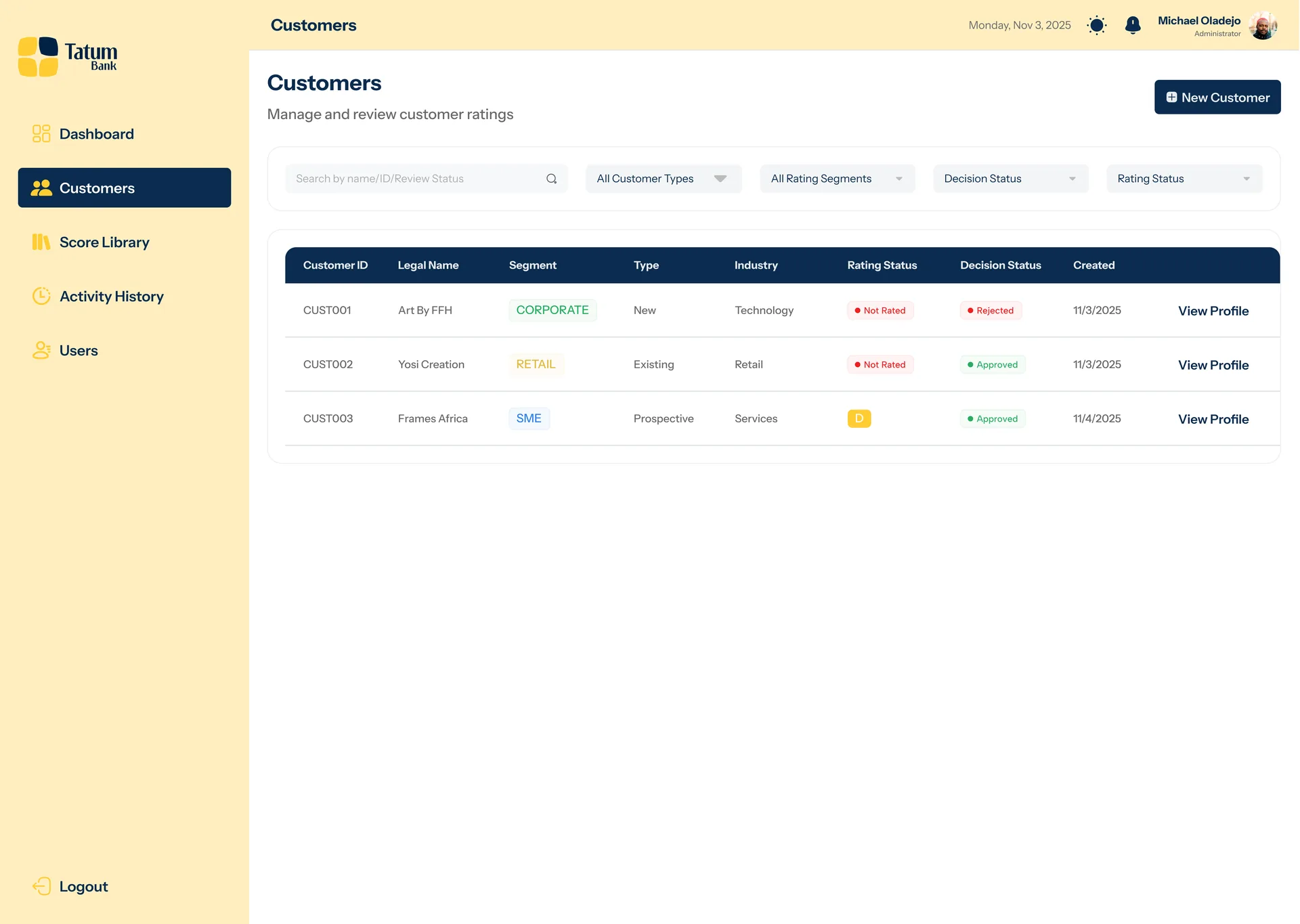

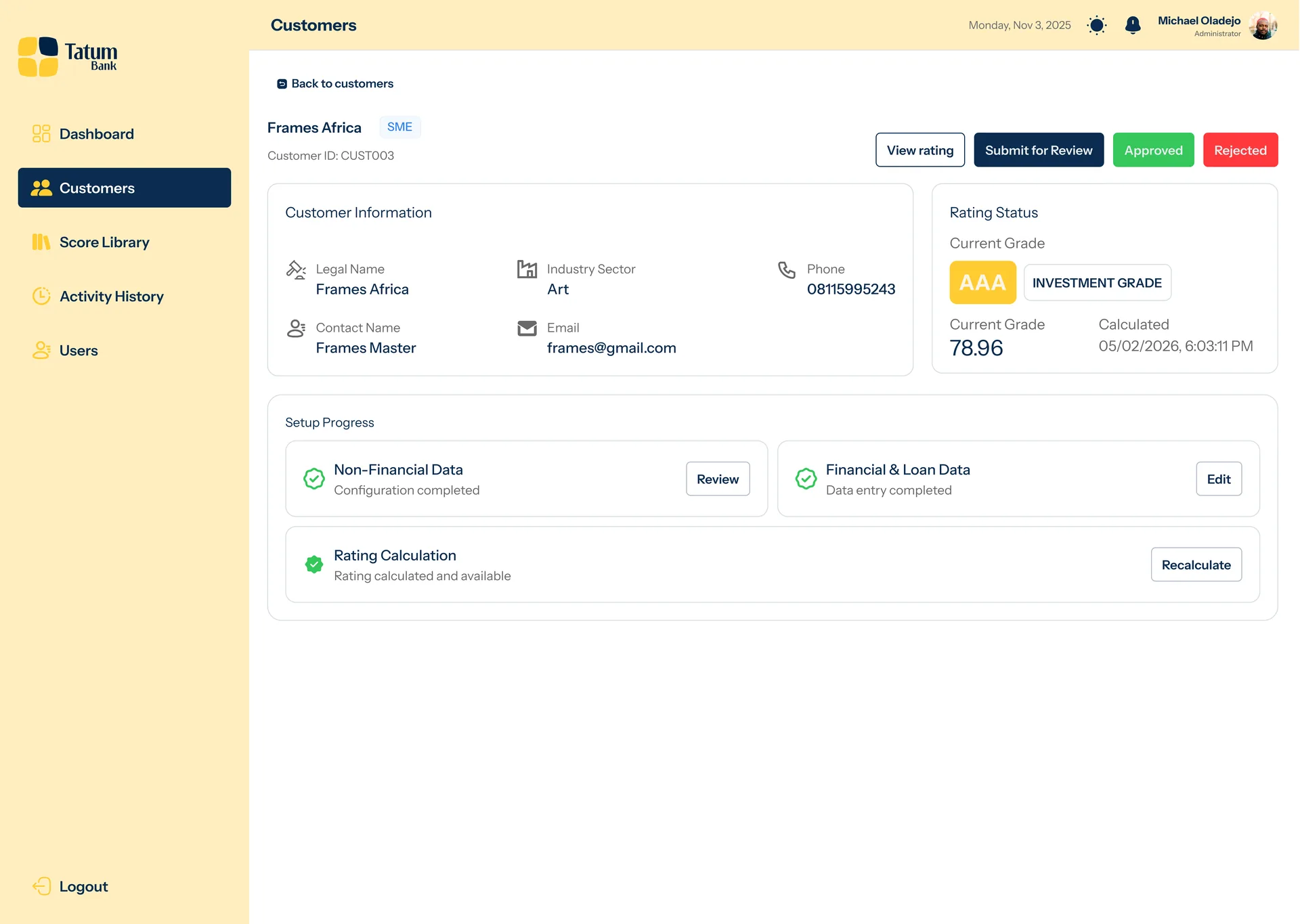

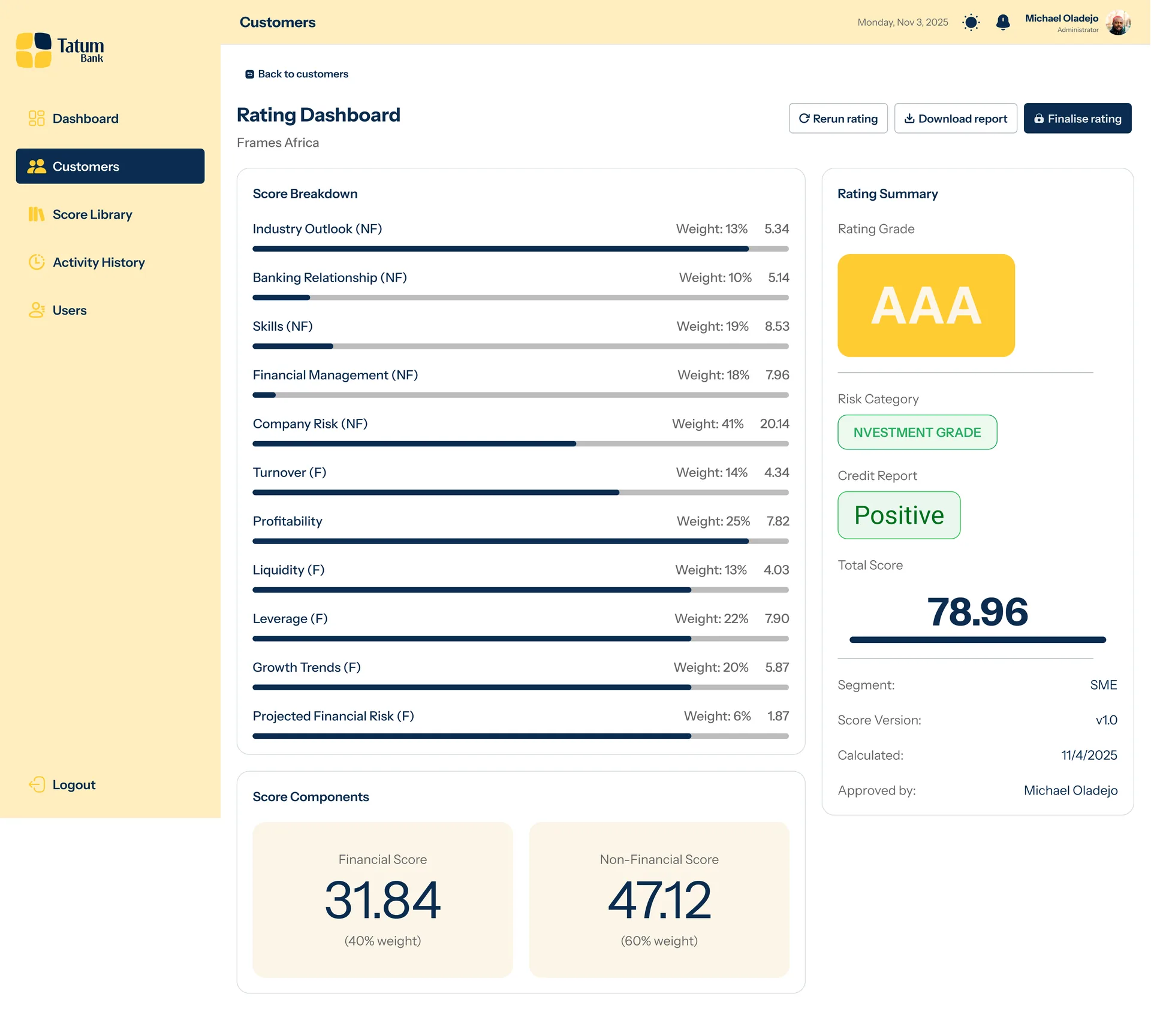

An obligor risk rating system for financial institutions. The platform assesses credit risk across three borrower segments (corporate, SME, and retail) using weighted combinations of financial metrics (gearing, profitability, liquidity, debt service) and non-financial factors (management quality, industry risk, regulatory exposure). Output is a structured grade from AAA to D, with clear score bands and reviewer routing built in.

My role.

Programme Manager

Problem context.

Credit risk assessment across most institutions was fragmented: each analyst worked from their own scorecard variant, reviews happened informally via email and side-channel approvals, and portfolio-level comparison was nearly impossible. The inconsistency made peer review difficult and audits harder still.

Decisions and execution.

Designed the system around a single canonical scorecard per segment, with explicit review states, routing rules, and an approval trail. Corporate, SME, and retail each have their own weighting logic, corporate weighs financials at 70%, retail at 40%, but all flow through the same governance workflow. Built portfolio reporting against the workflow itself so a senior risk officer's view came as a byproduct, not a downstream BI request.

Outcome.

Reviewers work from a single scorecard with clear status and traceable decisions. Coordination overhead dropped, portfolio visibility improved, and the grading output is consistent enough to support comparative analysis across the book.

What I would improve next.

Standardisation only lands when it feels like a constraint the team designed, not one imposed on them. Getting risk analysts into the scorecard logic early, before any UI existed, meant the weighting decisions were theirs.